How I Kept My Budget Calm During Exchange Semester — Real Talk on Staying Financially Stable

Studying abroad sounds exciting—new culture, new friends, new freedom. But when I landed in a foreign country as an exchange student, my wallet panicked before I did. Between unexpected costs and currency confusion, I almost blew through my savings in two months. What saved me wasn’t luck—it was learning how to balance spending with financial stability. Here’s how I turned my money stress into a smart, steady strategy—without sacrificing the experience.

The Hidden Financial Shock of Going Abroad

Many students dream of studying overseas, imagining vibrant cities, rich history, and the thrill of independence. What rarely makes the highlight reel, however, is the financial reality that hits within weeks of arrival. The cost of living abroad often exceeds expectations—not just in big-ticket items like rent or tuition, but in everyday purchases like groceries, public transport, and even coffee. What felt affordable back home can become a luxury abroad, especially when exchange rates shift unfavorably. This disconnect between expectation and reality creates a hidden financial shock that catches even the most prepared students off guard.

This shock isn’t just about numbers—it’s emotional. Being in a new environment, surrounded by new experiences, can trigger impulsive spending. The desire to fit in, to say yes to weekend trips, to dine at trendy cafes, or to buy souvenirs for loved ones back home can override rational budgeting instincts. Social pressure amplifies this effect. When friends suggest a spontaneous trip or a group dinner, declining can feel isolating. Yet each ‘small’ expense chips away at limited funds, and over time, these choices accumulate into serious financial strain.

One of the most common pitfalls is underestimating housing costs. Students often assume that university housing or shared apartments will be affordable, only to discover hidden fees, utility costs, or deposits that weren’t clearly outlined. Others find themselves in locations far from campus, leading to additional transportation expenses they hadn’t planned for. Similarly, public transit systems abroad may not offer student discounts, or the cost of a monthly pass may be significantly higher than anticipated. These seemingly minor oversights can derail a budget quickly, especially when combined with currency conversion fees that eat into every transaction.

The key to overcoming this shock lies in awareness. Recognizing that financial stress is a normal part of the exchange experience—rather than a personal failure—helps students approach money with more clarity and less shame. By acknowledging the emotional triggers behind spending and preparing for the true cost of daily life, students can shift from reactive panic to proactive control. This mindset shift is the foundation for everything that follows, from budgeting to banking to earning.

Building a Realistic Budget That Actually Works

A budget is only effective if it reflects real life. Many students create overly optimistic plans—allocating minimal funds for food, assuming they’ll cook every meal, or underestimating how often they’ll want to explore the city. These budgets fail not because the student lacks discipline, but because the plan itself is unrealistic. The solution is not stricter rules, but smarter design. A practical budget accounts for human behavior, local pricing, and the inevitable surprises that come with living abroad.

The first step is categorizing expenses into three clear buckets: essentials, flexibility zones, and personal treats. Essentials include rent, utilities, transportation, groceries, and insurance—non-negotiable costs that must be covered each month. Flexibility zones cover variable but necessary spending, such as dining out, phone plans, or school supplies. These categories should have soft limits, allowing room for occasional overages without guilt. Finally, personal treats—like concerts, travel, or shopping—should be budgeted as discretionary spending, with a fixed monthly amount that doesn’t compromise core needs.

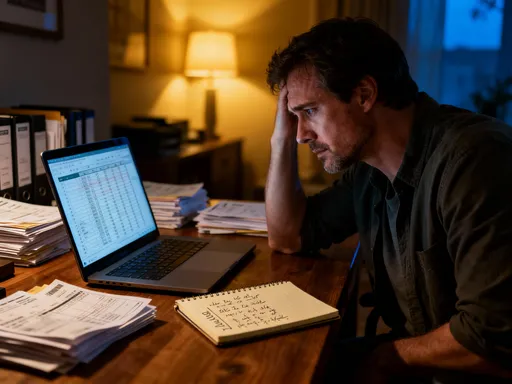

Tracking tools play a crucial role in maintaining this structure. Mobile apps that sync across devices allow students to log expenses in real time, often with automatic currency conversion. These tools provide instant feedback, helping users stay within their weekly limits. For example, setting a weekly food budget of $50 and receiving a notification when 80% of that amount is spent encourages mindful choices before the limit is exceeded. Some apps even categorize spending automatically, offering visual summaries that make patterns easier to understand.

Equally important is building in a buffer for emergencies. A flat tire, a medical co-pay, or a last-minute flight change can all lead to unplanned costs. Instead of pretending these won’t happen, a smart budget includes a small emergency fund—ideally 5% to 10% of total monthly spending—set aside specifically for unexpected events. This buffer reduces stress when surprises occur, preventing students from dipping into tuition money or relying on high-interest credit. By designing a budget that anticipates real-life challenges, students create a financial safety net that supports both stability and peace of mind.

Smart Banking for Cross-Border Living

Managing money across borders introduces complexities that go beyond simple withdrawals. Exchange students often face high fees for international transactions, delayed access to funds, or security risks when carrying large amounts of cash. The right banking strategy minimizes these risks while ensuring money is accessible, protected, and cost-effective. This begins with choosing financial tools designed for cross-border use, rather than relying on domestic accounts or tourist-friendly services that charge premium rates.

One effective approach is opening a local bank account, if permitted by visa status and university policy. A local account allows students to pay rent, utilities, and other recurring bills directly, often without conversion fees. It also simplifies receiving refunds, reimbursements, or payments from part-time work. Many local banks offer student-friendly packages with low or no monthly fees, online banking, and mobile apps in English. While opening an account may require documentation like proof of enrollment or a local address, the long-term benefits in convenience and cost savings are substantial.

For international transactions, using a debit or credit card with low foreign exchange fees is essential. Some global banks and fintech platforms offer cards that convert currency at interbank rates—the same rates used by financial institutions—without additional markups. These cards often come with no annual fee and can be linked to a primary bank account for easy top-ups. When withdrawing cash, students should prioritize ATMs affiliated with major banks over kiosks in tourist areas, which often impose excessive fees and poor exchange rates. Using a card that reimburses ATM fees adds another layer of protection against hidden costs.

Digital wallets that support multi-currency accounts are another valuable tool. These platforms allow users to hold funds in different currencies, convert them at favorable rates, and spend via linked cards or mobile payments. For students receiving money from family abroad, this means transfers can be made in their home currency and converted only when rates are favorable, avoiding the high fees of traditional wire services. Security features like instant card freezing, transaction alerts, and biometric authentication also reduce the risk of fraud. Together, these tools create a financial ecosystem that is both flexible and secure, tailored to the realities of international living.

Earning While Learning: Safe Side Income Streams

Financial stability during an exchange semester isn’t just about limiting expenses—it’s also about creating small, sustainable income streams. While full-time work is often restricted by visa regulations, there are legal and low-impact ways to earn extra money without compromising academic performance. The goal isn’t to become wealthy, but to cover incidental costs, build financial confidence, and reduce reliance on family support.

One of the most accessible options is online tutoring. Students fluent in their native language or skilled in subjects like math, science, or writing can offer virtual lessons to students back home or in other countries. Platforms that connect tutors with learners often handle payments, scheduling, and reviews, minimizing administrative work. Sessions can be scheduled during evenings or weekends, fitting around class hours. Earnings vary, but even a few hours per week can cover groceries, transportation, or small travel trips.

Freelancing is another viable path for students with marketable skills. Graphic design, content writing, translation, data entry, and social media management are in demand across industries. Websites that host freelance work allow students to create profiles, bid on projects, and receive payments internationally. While competition exists, students who deliver quality work and build positive reviews can establish steady client relationships. The key is to start small, set realistic goals, and avoid overcommitting time. Treating freelancing as a side activity—not a primary income source—ensures it complements rather than disrupts academic life.

On-campus opportunities should not be overlooked. Some universities offer paid research assistant roles, language exchange programs, or administrative support positions that accommodate student schedules. These roles often come with added benefits, such as access to campus resources, networking opportunities, or academic credit. Even short-term gigs, like helping organize events or translating materials, can provide modest income while enhancing the overall exchange experience. The common thread among all these options is sustainability—choosing work that fits within the student’s capacity and aligns with long-term goals.

Investing in Stability, Not Returns

When most people think of investing, they imagine stock portfolios, compound interest, and long-term wealth building. For exchange students, however, the concept of investment takes on a different meaning. Here, the priority isn’t growth—it’s stability. The real investment is in preserving capital, ensuring access to funds, and minimizing risk in an unfamiliar financial environment. This shift in mindset—from chasing returns to protecting value—is essential for students far from home.

Emergency funds are a cornerstone of this strategy. Instead of placing savings in high-yield but illiquid accounts, students should keep a portion of their money in easily accessible, low-risk vehicles. High-interest savings accounts, if available in the host country, offer modest returns with full liquidity. Alternatively, keeping funds in a digital wallet with instant transfer capabilities ensures money is available when needed. The goal is not to maximize interest, but to avoid penalties, delays, or losses when an urgent expense arises.

Another aspect of stability-focused investing is avoiding speculative behavior. The temptation to engage in foreign currency trading, cryptocurrency, or peer-to-peer lending can be strong, especially when peers talk about quick gains. However, these activities carry high risk and require expertise that most students lack. A single bad decision can wipe out months of careful budgeting. Instead, students should focus on financial safety—keeping funds in insured accounts, avoiding leverage, and steering clear of unregulated platforms.

This conservative approach may seem unexciting, but it serves a vital purpose. By prioritizing predictability over potential profit, students create a financial foundation that supports their academic and personal goals. They sleep better knowing their tuition is safe, their rent is covered, and they can handle surprises without panic. In this context, the return on investment isn’t measured in percentage gains, but in peace of mind, confidence, and the freedom to focus on learning rather than financial survival.

Avoiding the Most Common Money Traps

Even with a solid budget and smart banking habits, students face constant psychological pressures that can undermine financial discipline. Social events, travel opportunities, and the allure of new experiences create what behavioral economists call ‘present bias’—the tendency to prioritize immediate gratification over long-term consequences. Recognizing these traps is the first step toward resisting them.

One of the most pervasive traps is social spending creep. Saying yes to every dinner, concert, or weekend trip may seem harmless at first, but these costs add up quickly. What starts as a desire to bond with peers can turn into a pattern of overspending. The fear of missing out—FOMO—amplifies this behavior, making it hard to decline invitations even when funds are low. A useful strategy is the 24-hour rule: when faced with a non-essential purchase or event, wait a full day before deciding. This pause allows emotions to settle and rational thinking to return, often revealing that the expense isn’t as necessary as it first seemed.

Impulse buying in tourist zones is another common pitfall. Markets, souvenir shops, and duty-free stores are designed to trigger spontaneous purchases. Limited-time offers, attractive packaging, and the emotional high of being in a new place all lower resistance. To counter this, students can set a ‘fun budget’—a fixed amount allocated for souvenirs or small indulgences—and stick to it. Carrying only that amount in cash during outings reduces the temptation to overspend. Additionally, taking photos instead of buying trinkets can preserve memories without the financial cost.

Another trap is overestimating future income. Students may justify spending now with the belief that they’ll earn more later, whether through a future job or family support. This mindset leads to reliance on credit cards or borrowing, which can spiral into debt. Instead, grounding decisions in current reality—what is actually in the bank account today—creates a more sustainable financial habit. Visualizing long-term consequences, such as returning home with debt or missing out on post-grad opportunities due to financial strain, helps reinforce discipline. Awareness, not willpower, is the true safeguard against these traps.

Long-Term Gains: How This Experience Builds Financial Maturity

The value of an exchange semester extends far beyond academic credits and travel photos. For many students, it becomes a crash course in financial responsibility—one that yields lifelong benefits. Navigating budgeting, banking, and spending in a foreign environment builds resilience, decision-making skills, and confidence that translate into future financial health. These lessons don’t disappear after the program ends; they become embedded in how students manage money for years to come.

One of the most lasting impacts is improved budgeting discipline. Students who learn to track expenses, set limits, and adapt to changing costs develop habits that serve them in post-graduate life, whether they’re managing student loans, planning a household budget, or saving for a home. The experience of living within constraints teaches the difference between needs and wants, a distinction that remains relevant at every income level.

Risk awareness is another enduring skill. Having faced currency fluctuations, unexpected bills, and financial pressure abroad, students become more cautious and prepared in their financial decisions. They are less likely to fall for high-risk investments, more likely to build emergency funds, and better equipped to handle economic uncertainty. This awareness fosters a proactive rather than reactive approach to money management.

Finally, the experience cultivates a sense of financial independence. Students who successfully manage their funds abroad gain confidence in their ability to handle complex financial situations. They learn to research options, compare costs, and make informed choices—skills that are invaluable in adulthood. Whether dealing with insurance, taxes, or retirement planning, the foundation laid during the exchange semester provides a strong starting point.

In the end, studying abroad is not just about seeing the world—it’s about becoming someone who can thrive in it. The journey shapes not only cultural understanding but financial wisdom. By turning money stress into a structured, thoughtful practice, students gain more than stability; they gain the tools to build a secure, intentional financial future.